Some of the first ATMs obliged customers to insert cards representing set amounts. The cards were collected by the bank during business hours so the sums could be manually debited from customer accounts. These cards then had to be mailed back to each customer before they could be used again.

Banks, of course, kept iterating, and over 50 years later, we wouldn’t know what to do without our trusty “robot cashiers.” While Paul Volcker, Former Chair of the Federal Reserve called the ATM the "only useful innovation in banking", the last half-century, and particularly the last five years, has shown the banking industry to be open to embracing digital transformation despite regulatory headaches and security challenges.

Even more importantly, customers have more options and higher expectations than ever when it comes to banking products.

In this article, we’ll discuss the role of digital products and product management in the digital transformation of the banking industry, providing current examples of recent innovations in everything from mobile apps to blockchain.

The Changing Landscape of Product Management in Banking

The evolution from traditional to digital product management in banking reflects a broader shift towards more agile, customer-centric, and technologically advanced offerings. As banks navigate the tides of digital transformation, the role of the product manager has become increasingly central in bringing legacy products into the current day.

From Traditional to Digital: The New Era of Bank Product Management

Historically, product management in banking revolved around physical branches, face-to-face services, paper forms, and paper money. Today, digital transformation is reshaping this landscape, introducing a new era where convenience, speed, and personalized services dominate customer expectations.

Digital banking represents a fundamental change in how products are developed. This shift has led to the emergence of mobile banking apps, online payment systems, and AI-driven innovation, fundamentally altering the role and approach of product management in banking.

Key Responsibilities of a Modern Banking Product Manager

The modern banking product manager is at the intersection of technology, customer experience, and business strategy. Their responsibilities extend far beyond the traditional scope, encompassing:

Customer Insight and Market Research

Understanding customer needs and behaviors has never been more critical. Digital banking allows for the collection and analysis of vast amounts of customer data, providing insights that can drive product innovation and personalization. The role of a product manager now includes leveraging this data to anticipate customer needs and tailor banking services accordingly.

FREE Product Analytics Micro-Certification

Are you struggling to translate data into decisions? Become the data-savvy Product Manager every team need with our free micro-certification in Product Analytics.

Enroll Now

Digital Strategy and Innovation

Today's banking product managers must be adept at digital strategy, constantly exploring new technologies and platforms to enhance service delivery. This involves not only keeping pace with technological advancements but also foreseeing digital trends that can impact the banking sector. Innovations like blockchain, AI, and machine learning are redefining banking services, from security protocols to personalized customer interactions.

Cross-functional Leadership

Digital product management in banking requires a collaborative approach, bringing together teams from IT, marketing, customer service, and compliance. Product managers must lead these cross-functional teams to ensure cohesive product development and launch strategies that align with the bank's overall digital transformation goals.

Performance Metrics and KPIs

In the digital domain, product success is continuously monitored through a range of metrics, from user engagement rates to transaction volumes. Modern product managers are responsible for defining these KPIs, tracking performance, and iterating on products based on data-driven insights.

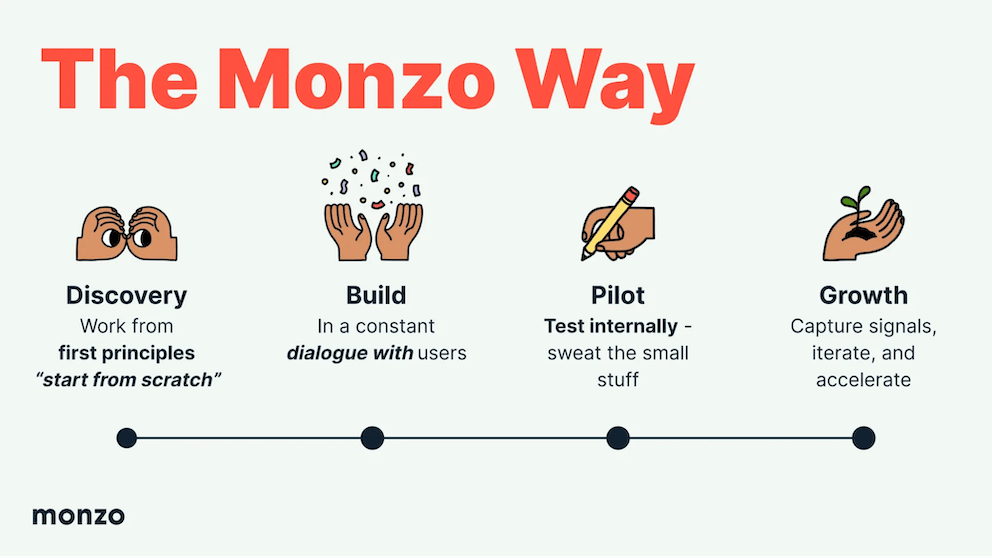

The “Monzo Way”

We were fortunate enough to host a talk by fintech disruptor Monzo’s CPO Fernando Fanton at ProductCon London who broke down the process for developing and implementing digital products at Monzo.

Tackling Unique Challenges in Bank Product Management

According to McKinsey Digital, only 30% of banks successfully implement their digital strategies. Let’s look at why.

Navigating Regulatory and Compliance Complexities

The banking sector is one of the most heavily regulated industries, with regulations that can vary significantly across different jurisdictions. Digital banking products, which often transcend geographical boundaries, must comply with a complex web of regulatory requirements, including everything from data protection laws to anti-money laundering (AML) standards and Know Your Customer (KYC) protocols.

Ensuring compliance while also striving to innovate and meet customer expectations for speed and convenience is a tightrope walk that many banks struggle with.

Balancing Innovation with Security in Banking Products

Innovation in banking, especially in the realm of digital products, must always be balanced with the paramount need for security. As banks introduce new technologies like blockchain, mobile banking apps, and online payment systems, they also open new vectors for cyber threats.

This dual mandate of driving innovation while safeguarding against security breaches requires a sophisticated approach to product development and management, where security is embedded at every stage of the product lifecycle, from conception to delivery.

High Technical Debt and Lack of Product Professionals

Many banks are burdened with high technical debt, a consequence of legacy systems that are deeply entrenched in their operational infrastructure. Modernizing these systems without disrupting ongoing services is a significant challenge that requires substantial investment and expertise.

Compounding this issue is the talent gap; there is a pressing need for professionals who not only understand the complexities of banking but are also adept at leveraging digital technologies to create user-centric products. While many banks know how to hire and reskill professionals with financial expertise, they are learning that they need to apply equal effort on attracting financial product professionals as well as developers and product marketers.

Emerging Trends Shaping Product Management in Financial Services

The percentage of customers who use online banking services daily increased from 1.5x in just one year from 2021 to 2022. Customers no longer see online banking as a “nice to have.” It’s a necessity. Not only that, the process should be frictionless, personalized, and delightful.

Personalization at the Forefront of Banking Services

We live at a time where personalization is not just preferred; it's expected. In banking, this means moving beyond one-size-fits-all products to offering services tailored to individual customer preferences, behaviors, and financial goals.

Advanced analytics and big data play pivotal roles here, enabling banks to understand their customers at a granular level and craft personalized banking experiences. This trend towards personalization enhances customer satisfaction, fosters loyalty, and differentiates banks in a competitive marketplace.

Leveraging AI and Machine Learning in Bank Product Management

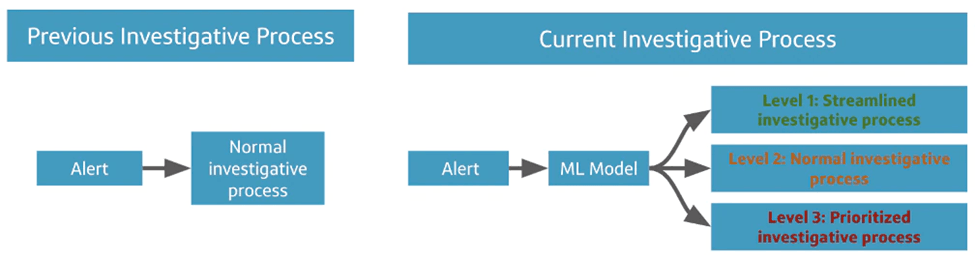

Capital One has transformed itself into an AI-first financial institution, leveraging machine learning across various aspects of its business, including customer service, call center operations, and fraud detection. Their AI-powered personal assistant, Eno, provides customers with a range of services such as balance checks, bill payments, and real-time fraud alerts.

Capital One’s Machine Learning Team built an interference engine to link up siloed datasets within the various components of its mobile app features. The bank also uses machine learning as the basis for a much more efficient fraud detection process than the previous rule-based one.

Image courtesy of HBS Digital Initiative

Blockchain Innovations at JPMorgan Chase

It’s not all technical debt and lack of talent! There are plenty of examples of traditional financial institutions that are leading the way for the rest of the industry in terms of digital transformation.

JPMorgan Chase has invested heavily in technology to improve its banking services. They have been pioneers in using blockchain technology to enhance customer service and security. For example:

JPMorgan Chase introduced the JPM Coin, a digital token that facilitates instant payment transfers between institutional clients. The JPM Coin operates on blockchain technology, ensuring secure and efficient transactions. It represents one of the first digital currencies to be backed by a major bank, with each coin equivalent in value to one US dollar.

The IIN (Interbank Information Network) is a blockchain-based network developed by JPMorgan to optimize the payment process and address challenges related to global payments, such as delays caused by compliance checks, errors, and other inefficiencies. By leveraging blockchain, the IIN allows member banks to exchange information in real time, facilitating quicker resolution of payment issues and smoother transaction processing.

Driving Growth through Mobile Banking at BBVA

BBVA (Banco Bilbao Vizcaya Argentaria, Spain): BBVA has been at the forefront of digital banking in Europe, focusing on digital transformation initiatives like open banking, mobile banking services, and the acquisition of fintech startups to enhance their digital offerings.

A significant aspect of BBVA's success has been its focus on creating a unified brand and experience across all digital and physical channels, a massive endeavor involving over 4,000 employees and described as one of the biggest projects in the bank's history.

This initiative not only revamped BBVA's global brand but also instilled a culture of collaboration and agile methodology within the organization, allowing employees from various departments to think like designers and work cohesively toward innovative solutions.

BBVA has established what it calls the "golden triangle" of collaboration between business, technology, and design. This approach has been instrumental in integrating customer insights into every stage of product development, leading to the creation of services that are not only technologically advanced but also highly user-friendly.

BBVA's mobile app, for example, was recognized by Forrester as the best banking app in the world for three consecutive years, thanks to its superb balance between functionality and user experience. BBVA's commitment to digital transformation is evident in its growth statistics, with more than half of its active customers now engaging with the bank via mobile devices.

Essential Skills for the Future Banking Product Manager

The evolving landscape of banking, shaped by digital transformation, demands a new set of skills for product managers, including proficiency in one or more of the following specializations:

Data analytics

Digital platforms

AI and machine learning

Blockchain

Equally important are soft skills such as agile leadership and cross-functional collaboration, as product managers often lead diverse teams to drive digital initiatives.

Transitioning to digital-first banking requires more than just technical skills; it necessitates a cultural shift within the organization. Banks must cultivate an environment that encourages innovation, where failure is viewed as a stepping stone to success and continuous learning is embedded into the fabric of the organization.

Initiatives such as internal hackathons, innovation labs, and partnerships with fintech startups can stimulate creative thinking and fast-track the development of digital solutions. Moreover, providing employees with access to digital skills training and professional development opportunities ensures that the workforce remains adaptable and prepared for the challenges of digital banking.

Master Digital Transformation Strategies

Only Product School brings you Product Advisors and instructors with the proven experience to accelerate your transformation.

Learn more

Updated: May 6, 2024